Under UAE VAT, the first VAT return is due on 28th Feb, 2018, which will be filed by those businesses for whom the monthly VAT return is applicable. The businesses are required to file VAT Return online using the Federal Tax Authority (FTA) portal. The FTA portal is designed to accept the returns only through online mode as offline capabilities to file VAT return through XML, EXCEL or any other utility are currently not available. This implies that the taxpayer is required to manually provide the values of Sales, Purchase, Output VAT, Inputand Input VAT etc. in the appropriate boxes of the VAT return form available in FTA portal.

The VAT Return form is named as ‘VAT 201’ which the taxpayer needs to fill and submit in order to complete the VAT Return filing. The Form VAT 201 is broadly categorized into 7 sections as mentioned below:

Each of these sections contain various boxes in which the taxpayer needs to furnish the details in order to complete the VAT Tax return filing. Each of the above sections and the details required to be furnished in relevant boxes of VAT Return Form 201 are discussed below:

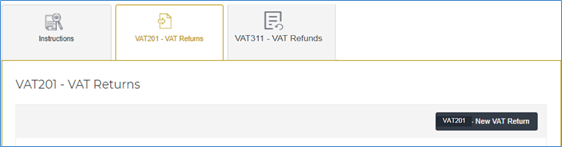

To access the VAT Return Form 201, the taxpayer should log in to the FTA e-Services portal using your registered username and password. Form Navigation menu, select the ‘VAT’->VAT 201- VAT Return-> click on ‘VAT 201-New VAT Return’ to initiate the VAT return filing process.

On clicking ‘VAT 201- New VAT Return’ as shown in the above image, various sections of VAT return form will open. Let us discuss the step by step process involved in filing the VAT Tax return along with the information required to be furnished in each of the following sections.

In the above section, details such as the “TRN” or “Tax Registration Number” of the taxpayer, as well as their name and address will be captured. These details will be auto-populated.

In case of tax agent submitting the VAT return on behalf of a taxpayer, the details of TAAN (Tax Agent Approval Number) and the associated TAN (Tax Agency Number) along with the Tax Agent and the Tax Agency name are populated at the top of the VAT Return.

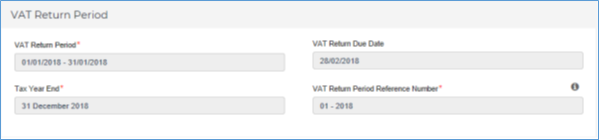

The details in the above section such as VAT return period for which you are currently filing a return, the Tax Year end, VAT return period reference number and VAT return due date will be auto-populated.

The tax year end is important for businesses who are not able to recover all of their input VAT and need to perform an input tax apportionment annual adjustment. Such adjustment is allowed only in the first return following the tax year end. VAT return period reference number indicates the VAT return period which you will be completing within that tax year.

If the VAT return period reference is 1, those affected businesses should include their input tax apportionment annual adjustment in that VAT return. Businesses need not worry now, because this is applicable after 1st year of VAT return i.e. from 1st January, 2019 onwards.

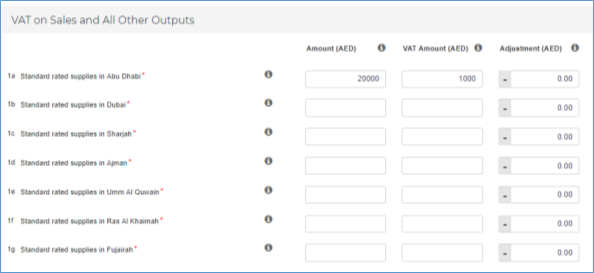

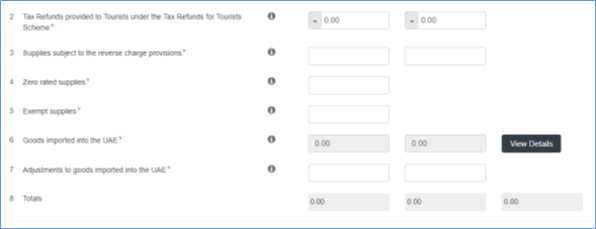

In the above section, you need to furnish the details of standard rate taxable supplies at the Emirates level, zero rate supplies, exempt supplies, supplies subject to reverse charge mechanism etc.

In the above section, you need to furnish the details of purchases or expenses on which you have paid VAT at a standard rate of 5% and supplies subject to reverse charge basis along with the eligible recoverable input tax.

This section indicates your VAT payable for the VAT return period. The box number 12: Total Value of due tax for the period indicates the total value of output tax that is due for the Tax Period. This will be calculated based on the information declared in Sales and all other outputs. This will be the sum of the Output VAT and Adjustments columns in the Sales and all other outputs.

Similarly, box number 13: Total value of recoverable tax for the period indicates total value of Input Tax that is recoverable for the Tax Period. This will be calculated based on the details furnished in VAT expenses and all other inputs section. The box number 14 indicates the payable tax for the period. This will be the difference between the total tax due for the period and the total recoverable tax for the period. Either it will result in net VAT payable or recoverable tax.

If the amount in Box 12 is more than the amount in Box 13, the difference is the amount of VAT that you must pay. If the amount in Box 12 is less than the figure in Box 13, then you will be eligible to request a refund for the net amount of recoverable tax or carry it forward to the subsequent VAT return period.

This section is applicable only for businesses who have used and applied the provisions of the Profit Margin Scheme during this period. Else, you can tick ‘No’ and proceed to the next section. This is just an additional reporting which does not have any financial impact on your VAT Return.

In the above section, provide the authorized signatory details and tick the box next to the declaration section to submit the VAT Return. The taxpayer also has an option to save the details as a draft and submit it later.

Before submitting the VAT Return, the taxpayers have to take utmost care in verifying all the details and only when he or she is certain that all the information is correct, click the submit button. After the successful filing of the VAT Return, a taxpayer will receive an e-mail from FTA confirming the submission of VAT return form.

The UAE VAT return filing requires the details required at a summary level meaning the consolidated details of Sales, Purchase/expenses, output VAT and Input VAT. More importantly, the details need to be consolidated accordingly to the format as prescribed by the Federal Tax Authority (FTA). If you closely observe, in certain boxes, the detailing is not just the consolidation of sales or purchases. Instead, it requires a sub-level detailing or declaration of details based on the eligibility. For example, standard rated sales are required at the Emirates level, the taxpayer is required to furnish only those expenses or purchase on which he is eligible to recover the input VAT etc. It will be highly difficult for business to manually collate and compile transactions for filing VAT Return and by doing so, you will be running the risk of missing deadlines which eventually lead to non-compliance. Thus, it is a must for businesses to have the right tax accounting software which will not only help you to account your VAT transactions but also triangulate your business records to generate the accurate VAT Return in the prescribed format. By having a right Tax accounting software, businesses can easily generate the accurate VAT Return with zero or minimum efforts and more importantly, avoid the hefty penalties ranging from AED 1,000 to 3,000 for non-filing or incorrect filing of VAT Returns.

For businesses, a tax accounting software will play a key role in defining the success of a business in the field of compliance adherence. The businesses need to carefully evaluate the software which will help in hassle-free transition of your businesses into a new VAT regime, ease of accounting VAT and filing returns.

Process of Filing VAT Return in UAE – VAT Return Form 201

To access the VAT Return Form 201, the taxpayer should log in to the FTA e-Services portal using your registered username and password. Form Navigation menu, select the ‘VAT’->VAT 201- VAT Return-> click on ‘VAT 201-New VAT Return’ to initiate the VAT return filing process.

For More Details on visit us on www.alyaauditors.com VAT please write us to audit@alyaauditors.com,bibin@alyaauditors.com or Talk to us : Tel: +971 4 876 9377, Mob: +971 52 475 4007, +971 52 975 0690