The UAE introduced Economic Substance Regulations to honour the UAE’s commitment as a member of the OECD Inclusive Framework on BEPS, and in response to a review of the UAE tax framework by the EU which resulted in the UAE being included on the EU list of non-cooperative jurisdictions for tax purposes (EU Blacklist). The issuance of the Economic Substance Regulations on 30 April 2019 (the Regulations), and the subsequent release of the Guidance on the application of the Regulations on 11 September 2019, was a requirement for the removal of the UAE from the EU Blacklist on 10 October 2019. The purpose of the Regulations is to ensure that UAE entities that undertake certain activities (see question 4) are not used to artificially attract profits that are not commensurate with the economic activity undertaken in the UAE.

Purpose of the ESR

The main purpose of the ESR is to comply and bring specific requirements for the entities incorporated in the UAE to demonstrate that the companies are carrying out the actual economic activity in the State that achieve economic substance interest and the basis to support that the incorporation in the UAE was not driven solely to benefit from the privileged tax regime.

The introduction of the ESR in the UAE brings the UAE in line with other jurisdictions that have recently issued economic substance legislation (e.g. BVI, Mauritius, Cayman Islands, Bermuda Bahamas, Guernsey, the Isle of Man and Jersey), and affirms the UAE’s commitment to addressing concerns around the shifting of profits derived from certain geographical mobile business activities to “no or nominal tax jurisdictions”(called as “NOON’s”) without corresponding local economic activities. Such type of companies uses NOON’s to park profits thereby harming the tax base of another jurisdiction.

The introduction of the ESR in UAE is one of the milestones for the UAE’s tax policy and it is an important step towards its affiliation with the global Organization for Economic Co-operation and Development’s (OECD) Base Erosion and Profit Shifting (BEPS) directives. Aside from this, the implementation of the Regulation should further strengthen and benefit the UAE in helping and assisting to address various reputational concerns such as in respect of transparency, which the jurisdiction has been subject to from international players and investors alike.

Who is subject to the ESR ?

The Regulations shall apply to all UAE onshore, free zone and offshore entities that carry on a “Relevant Activity” to be within the scope of the Regulations. However, whether ESR shall applicable to the sole proprietorship or branch office shall yet to be clarified.

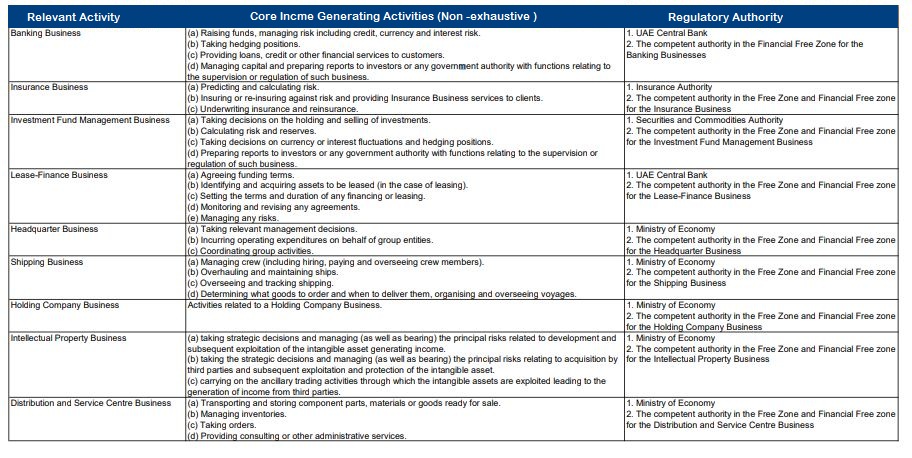

Which are the relevant activities under ESR ?

The following are considered as “Relevant Activities” under the Regulations:

- Banking

- Insurance

- Fund management

- Lease-finance

- Headquarters

- Shipping

- Holding company

- Intellectual property (IP)

- Distribution and service centre

Economic Substance Test in the UAE

The economic substance test is based on the three important key pillars that a Licensee/Company must satisfy the following criteria to meet the Economic Substance Test in relation to any Relevant Activity, as specified above, carried on by it.

- Core Income Generating Activity (“CIGA”) related to the activities covered by the ESR should

be undertaken in the UAE;

- Licensee/Company should be directed and managed from the UAE;

- The Licensee’s activities must be carried out with adequate local “Economic Substance” with regard to the level of relevant activity in the UAE.

The Economic substance consists of:

- Full-time employees

- Expenditure

- Premises

Which are the core income generating activities (CIGA) as per ESR ?

According to Article 5 of the Regulations, State Core Income-Generating Activities means activities that must be conducted by a Licensee in the State (UAE) and shall include:

Economic Substance Regulation Submission in UAE

What ALYA Auditors offers?

- Consulting on ESR

- Identify the qualifying entities for ESR compliances

- Identify the qualifying business segments for ESR compliances

- Report and advise on overall ESR readiness by the Entity

- Ongoing ESR compliance

- Secretarial services in connection with ESR record maintenance

- ESR filing with the authorities in the proper /prescribed format

Ready to Start?

Talk to a UAE compliance expert

Book a free, no-obligation consultation with ALYA Nexus Auditing.

Book Free Consultation ↗