Economic substance rules were introduced in the United Arab Emirates (UAE) in April 2019, and businesses need to assess how they comply with those rules.

Economic substance regulations have recently been introduced across the globe in countries with no or nominal corporate tax rates in order to comply with international initiatives to combat harmful tax practices.

In essence the new rules require certain legal entities established in those countries to demonstrate that they carry out substantial economic activities there.

Who is subject to the Regulations?

What are the economic substance requirements?

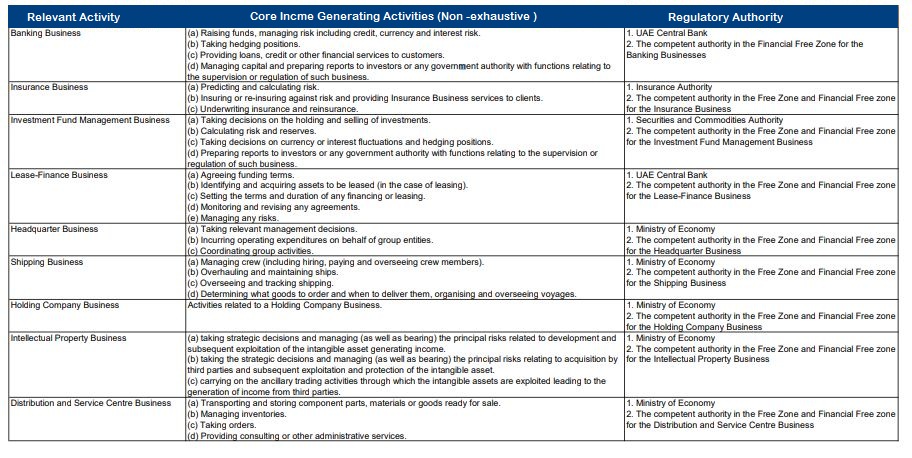

To satisfy the economic substance requirements in relation to a Relevant Activity, a Relevant Entity must:

● Conduct the relevant “core income generating activities” in the UAE;

● Be “directed and managed” in the UAE; and

● With reference to the level of activities performed in the UAE:

- Have adequate number of qualified full-time employees in the UAE

- Incur an adequate amount of operating expenditure in the UAE

- Have adequate physical assets in the UAE.

A Relevant Entity that only undertakes a Holding Company Business will be subject to less stringent economic substance requirements. Additional requirements apply if a Relevant Entity carries out “high risk IP related activities”. If a Relevant Entity carries out more than one Relevant Activity, the economic substance requirements must be met for each of the Relevant Activities.

What are Substantial Activities under Economic Substance Regulations?

Substantial Activities under Economic Substance Regulations means the Companies get incorporated under the local law of the country but do not engage or conduct any activity or hold any substance in that country. Generally, such practices are done in “No or Nominal Tax jurisdictions” (called as NOON’s). Such Companies use NOON’s to park profits thereby harming the tax base of another jurisdiction.

Therefore, Forum of Harmful Tax Practices (FHTP) conducts reviews to check whether the practices of one jurisdiction is harmful to the tax base of another jurisdiction. One of the areas of FHTP is Substantial activity requirements. To prove the substance of the activities undertaken by Company in the Country is important to have a clear view and information on the amount of business conducted from that jurisdiction. This becomes important for such companies having their head office in country where the global income gets taxed. Hence it is necessary to prove the substance of the activities carried.

Has your Relevant activity complied with Economic Substance Test

- The Economic substance test is required to be met for each relevant activity by conducting the Core-Income Generating Activities (CIGA) in UAE. The list of activities is provided by regulation for CIGA, but it is not exhaustive list. It is clarified that CIGA includes the activities listed in the regulation, but the list is not restricted to those activities. We assume that any incidental or ancillary activities in relation to the main relevant activity will also take the color of relevant activity and fall under the list of CIGA.

- It is stated that the business of the licensee should be directed and managed in UAE, which means the board meetings should be held in UAE. Further, the quorum of the meeting, minutes of meeting duly signed by the directors attending the meeting need to be maintained. Physical presence & Expertise of the Directors is mandatory requirement. It is also made clear that atleast one meeting in one Financial Year or as required by the law applicable to the Licensee should be conducted in UAE for discussing the matters of the Company.

In cases where Companies are managed by Manager & CEO, the requirements shall apply to that concerned Manager or CEO. Also, the responsibility lies with the licensee to prove that the Manger or CEO has relevant knowledge and expertise to take decisions and merely acting on the decisions taken outside UAE.

iii. One of ESR test is to have adequate number of qualified employees to conduct licensee activities. Adequate number will depend on the nature and the size of Business of Companies. Again, the responsibility lies on the licensee to prove to the regulatory authority the genuineness of the activities with the available Employees, Operating Expenditure and Assets.

- Licensee Company carrying on relevant activity must incur adequate Operating Expenditure, should have adequate Physical Assets and appropriate Premises to conduct business. Again, what is adequate & appropriate will depend on the nature and the size of Business of Companies. It is made very clear that Licensee has to maintain all the records and should be in a position to prove or demonstrate the adequacy & appropriateness of its Expenses & Assets.

These requirements are to be satisfied to prove that the licensee holds substance and the business are genuine.

Details on what will be included in the State Core Income-generating Activities for the above mentioned 9 relevant activities will be followed in our future blog.

Does your business fall under Economic Substance Regulations in the UAE?

If your business falls under the entities with the above-mentioned activities in the UAE, then you may need assistance to determine the applicability if Economic Substance Regulations is relevant for you as you need to analyze the implication of this new regulation in the UAE.

The team at ALYA Auditors will assist you in making this determination; provide preliminary assessments of your company’s current compliance obligations, and assist with possible future strategies, in response to this new legislation.

For Economic Substance Regulations in the UAE

Ready to Start?

Talk to a UAE compliance expert

Book a free, no-obligation consultation with ALYA Nexus Auditing.

Book Free Consultation ↗